Digital 9 Infrastructure ($DGI9.L): Liquidation

Trading at a ~73% discount to last reported NAV

This post analyses a listed private-equity style closed-end fund in the process of selling its assets. Shares are trading at a wide discount to the last reported indicative NAV and to conservative estimates of liquidation value.

This is an in-depth post and is restricted to paid subscribers - please subscribe or upgrade below to read (free trial available).

Digital 9 Infrastructure ($DGI9.L) is a ~£190m market cap listed closed-end fund focused on digital infrastructure that is currently in the wind-down mode. Shares are currently quoted at around 21p vs a reported NAV of 79p as at Dec-23 (~73% discount).

Situation Overview

The fund was listed on the London Stock Exchange in March 2021, raising £300m in initial proceeds, and is managed by a London-based investment management firm Triple Point. Upon listing, Digital 9 acquired an operator of transatlantic subsea fibre cables (Aqua Comms), followed by investments in data centres (Verne Global), a fixed wireless provider (Host Ireland, now renamed as Elio Networks) and, finally, a 52% economic stake in the UK’s TV broadcast infrastructure operator (Arqiva).

The acquisitions and follow-on investments were initially financed by equity raises (~£900m in total, including the IPO), however eventually the fund started borrowing on a £375m fund-level short-term RCF, which was intended to be refinanced with debt at operating company level. By the end of 2022, Digital 9 stretched itself to the limit when it resorted to a vendor loan to finance the Arqiva investment. As interest rates began to rise and investor sentiment towards infrastructure turned a few months later, the fund exhausted its RCF capacity and started to feel pressure from lenders and shareholders. This forced it to begin selling assets and ultimately to commence a managed wind-down (recently approved by shareholders).

The fund has now completed the sale of one of its larger holdings - the data centre group Verne Global - for up to ~£450m including a ~£106m earnout (a mild 5% discount to Jun-23 valuation, but only if the earnout is fully achieved). The initial proceeds of £326m allowed the fund to reduce the RCF which will now have only ~£53m outstanding (due in March 2025).

Portfolio Valuation

The table below summarises the fund’s portfolio as at Dec-23 based on an independent valuation commissioned by the Board (with Verne Global valued at cash proceeds + deferred consideration + discounted earnout and with RCF before repayment):

The reported NAV based on this valuation came in at £686m or 79p/share, however it included the Verne Global earnout (discounted to £27m) and some fairly bullish valuations for the remaining assets, as discussed below.

Portfolio Assets

Let us briefly review each of the remaining assets:

Aqua Comms: An independent owner/co-owner and operator of transatlantic subsea fibre communication cables (6 pairs at ~20 TPBS each), as well as UK-Ireland and UK-Denmark interconnect cable systems. Some cable pairs are leased to content providers (FAANGs) on life-of-cable leases (IRU), providing a stable revenue base, while the rest of the capacity is being offered on shorter terms. Revenue has been growing at single digits in recent years, however 2023 EBITDA was depressed by new sales hires, network operations internalisation and backhaul investment for the recent launch of a third transatlantic cable (2023 margin was 30% vs ~50% average in previous years). The business was acquired by Digital 9 for ~12x EBITDA in 2021, when fibre acquisition multiples were approaching 20x. However, the fibre asset prices have reportedly fallen back to 10-14x now and the independent valuation looks fairly ambitious in this context, even assuming future margin recovery. The fund’s valuation is based on the operating company’s business plan and is based on continued growth in capacity demand, likely supported by the expected decommissioning of the cables built during the dotcom boom in the next few years. It also apparently includes some upside from a planned expansion to Asia, which looks far-fetched and is in the nascent stages. In any case, the valuation increase from the original £170m investment looks questionable in the current environment.

EMIC-1: A new cable system connecting Europe, the Middle East and India being laid by Aqua Comms, valued at cost as it is still in development. It is expected to launch in 2025, however may be delayed by the geopolitical tensions in the region.

SeaEdge UK1: A data centre and cable landing station building leased to a data centre operator on a long-term lease. Valuation is based on a real estate broker’s estimate (implied 7% cap rate).

Elio Networks: Owner and operator of a fixed wireless access network in Dublin, offering wireless broadband to business and government customers. The business was acquired for ~£50m in 2022 and has been growing at 6% p.a. in the last two years with 50%+ EBITDA margins. Given the decline in the transaction multiples in the infrastructure sector, however, this asset’s valuation may turn out to be somewhat ambitious as well (indeed, an open access fibre operator in Ireland was acquired at 8.3x EBITDA last year - see here).

Arqiva: UK’s national operator of broadcast towers for TV and radio transmission, as well as satellite uplink infrastructure. The TV/radio distribution business is stable to declining, so the company diversified into connectivity for smart water meters and other utility sensors and this new segment has grown 20% in FYE Jun-23 to 29% of revenue. EBITDA, however, has been stagnating, partly due to increasing energy costs. Digital 9 bought its stake in Arqiva from CPPIB in 2022 and acknowledges that it may be the toughest to sell, as the original sponsor Macquarie (still owns 26.5%) had been attempting to exit for several years without much success. Nevertheless, the valuation looks in line with listed comparable Rai Way ($RWAY.MI) which trades at 8.8x EV/EBITDA, albeit Arqiva is more levered (at 5.4x) and there is extra leverage on the Digital 9’s stake through the (non-recourse) VLN.

Governance

DGI9’s Board now comprises only independent directors, with no representation from Triple Point. Two additional independent directors with fund wind-down experience were appointed recently, but have resigned shortly after, leaving lingering doubts about the fund’s governance (which may be a source of the discount to NAV). However, despite a fairly dispersed shareholder base, some dissatisfied investors led by Aqua Ventures, a ~3% shareholder and previous owner of Aqua Comms, had gone activist on the Board and the investment manager, pushing the strategic review through and are now likely monitoring the situation closely. The fund is also currently recruiting a permanent chair and a new independent director to support the wind-down.

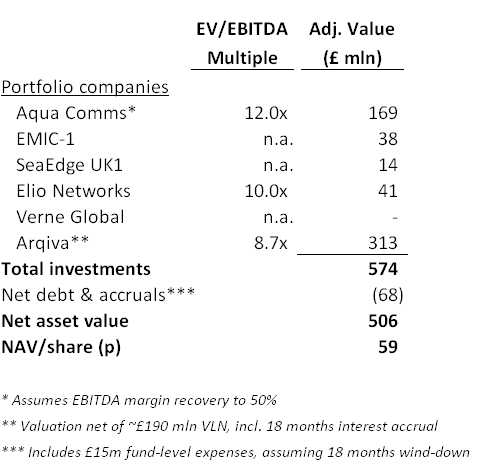

Liquidation Value

To address some of the points raised above, the table below attempts to estimate a conservative liquidation value for DGI9 (pro-forma for the Verne Global disposal and partial repayment of the RCF):

Based on the above assumptions, the liquidation value comes down to ~£500m or 58.5p/share, which still leaves a substantial upside to the current market price. It should be noted, however, that value realisation would take some time (possibly a couple of years) and DGI9 will have to progress the asset sales and fully repay the RCF before any distributions could be made to shareholders.