Alfa ($ALFAA.MX): Recent Spin-Off RemainCo

Defensive business at a discount; expected re-rating following structural simplification

This post covers:

A recent mid-cap spin-off situation;

Defensive, quality business liberated from a cyclical one;

Trades at <7x EV/EBITDA, below peers.

Alfa ($ALFAA.MX)

Price: Ps.12.92 • M.Cap: MXN 71.8bn ($3.4bn)

Alfa is a former conglomerate that spun off a listed subsidiary, a plastics manufacturer Alpek ($ALPEKA.MX), on 4 April. The spin-off was the last in a series and resulted in the RemainCo owning only one main business - a packaged foods producer Sigma Alimentos. Inside Alfa, the food business historically traded at an implied discount to peers, and pro-forma for the spin-off, Alfa/Sigma is still trading at the lower end of the local comps range on EV/EBITDA1 basis, despite higher growth, with potential for a re-rating.

Sigma is a producer of branded packaged meats, as well as dairy and other products, operating in Mexico (48% revenues), Europe (26%), the US (19%) and some other Central/Latin American countries. It has strong market positions (notably ~50% market share in processed meats in Mexico) and good product diversification, established in part through a number of acquisitions. Sigma grew its volumes and revenues at a 5% and 9% CAGR over 2010-24, respectively, while generally maintaining its margins (see chart below).

Sigma Historical Growth and Margins

In 2024, Sigma generated $8.8bn revenue, $1bn adjusted EBITDA (11% margin) and ~$400m FCF (excl. growth capex). Going forward, management guides to mid-to-high single digit EBITDA organic growth, which looks achievable, based on the following drivers:

Continued core business growth, primarily through volume plus some inflation pass-through;

Margin expansion through cost-saving actions, portfolio optimisation and restructuring, primarily in Europe where margins have long lagged Mexico/US (in the single digits in recent years);

Product extension according to local opportunities (e.g. Hispanic-focused brands have been a growth driver in the US recently).

For the current year, the company’s guidance assumes a 4% volume growth and 10% revenue growth at constant exchange rates, but 5% EBITDA growth due to raw material cost pressures in the Americas (which emerged in Q4’24). At the same time, management plans to increase capex by ~40% for capacity expansion (as the existing plants are nearly fully utilised) and strategic initiatives in the next two years2.

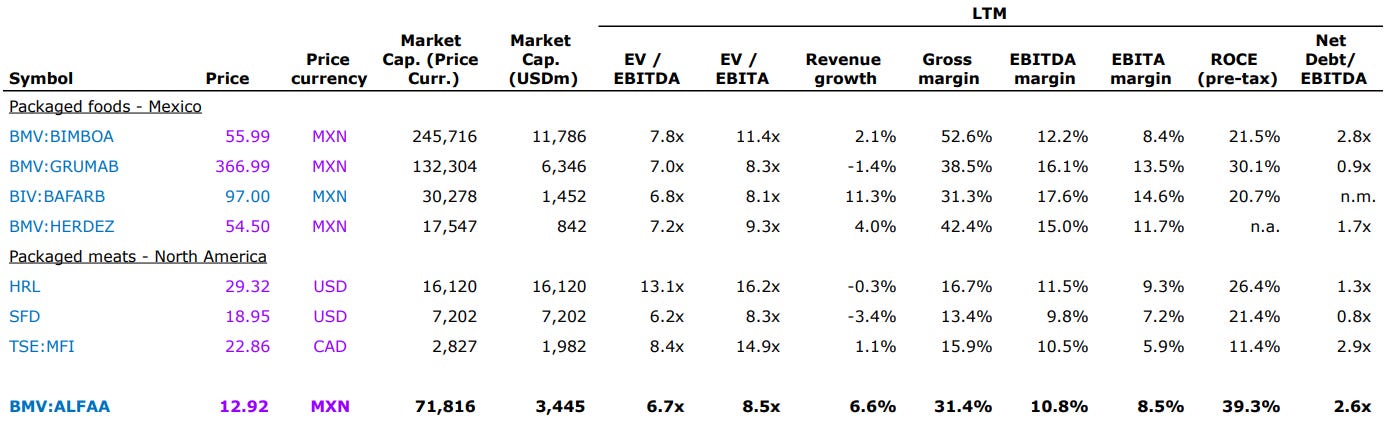

As mentioned above, Alfa/Sigma trades at the lower end of the range of the Mexican packaged food and North American packaged meats producer valuations (see table below).

The multiples could be explained by Sigma’s lower margins vs local peers, however the latter are not fully comparable, as Bimbo ($BIMBOA.MX) specialises in baked goods, Gruma ($GRUMAB.MX) in corn flour/tortilla, Herdez ($HERDEZ.MX) in canned products3, while Bafar ($BAFARB.MX) has a sizeable property investment business and trades on a secondary exchange. Sigma’s regional EBITDA margins (16% in Mexico and 13% in the US in 2024) are also in line with peers.

Moreover, Sigma’s relatively higher growth should arguably still earn it a multiple at least in line with larger Mexican peers, implying a ~20% relative upside if the valuation gap closes. This is also validated by a DCF valuation based on the current outlook (see at the end of the post).

A few other points about Alfa/Sigma are addressed below:

Sigma would not be directly affected by US tariffs on Mexican imports as it has US production capacity (8 facilities) and does not export to the US;

Alfa was previously seen as over-levered, however it managed to reduce debt towards a 2.5x net leverage target and achieve investment grade ratings through cash flow generation and an equity raise;

The company owns some prime land in Monterrey, reportedly worth “several hundred million dollars”, however there are no immediate plans to monetise it;

There are also MXN 7bn (~$350m) tax loss carry-forwards, a large part of which are in Spain;

No tax impact is expected from the spin-off, as any tax charge would be offset by the available tax losses in the HoldCo;

According to the management, there would be no material costs remaining from the HoldCo structure by the end of the year, and any remaining (small) non-Sigma operations will be shut down or divested;

The founding Garza Sada family owns ~30% and is very much in control, however no governance issues have surfaced so far and, in fact, their strategy has long been to “unlock value” and eliminate the historical conglomerate discount.

Key risks:

Potential recession in US/Mexico due to the US trade war which could lead to lower volumes and pricing pressure (although Sigma managed fairly well in 2020 with a 3% decline in volumes while still increasing prices vs a ~9% GDP contraction in Mexico) - hedging through a Mexico ETF or a peer basket could be considered;

Possible further margin pressure from higher raw material prices (raw meat and energy, partly denominated in USD) as Sigma appears to have only an opportunistic hedging strategy. The company can mitigate this through flexible global sourcing and pricing increases, however Sigma may not be able to fully pass the costs onto consumers in a challenging economic climate;

Potential market share losses to private label in the US/Mexico, where it accounts for ~20%/30% of retail (vs ~40% in Europe), but is growing on the back of cost-of-living pressures and may accelerate further.

Important reminder: The above publication is for information only. None of the mentions in this post are intended nor should be construed as investment recommendations or offers to buy or sell any securities. Please do your own due diligence and manage your risk appropriately. You should also assume that the authors hold positions in the securities of the companies mentioned and may trade, enter or exit the positions at any price.

Pre-IFRS 16

Note that this guidance was issued before the April US ‘reciprocal’ tariffs announcement (though after the initial US tariffs on Mexican imports announcement in February).

Herdez also does not fully own its main businesses - its operations are structured as 50/50 JVs with international partners, making analysis complicated.